A Broad Selection of Accounting Courses

Build skills with courses, certificates, and choose suitable online video courses with new additions published every month.

Search Courses.

Job Guaranteed Courses

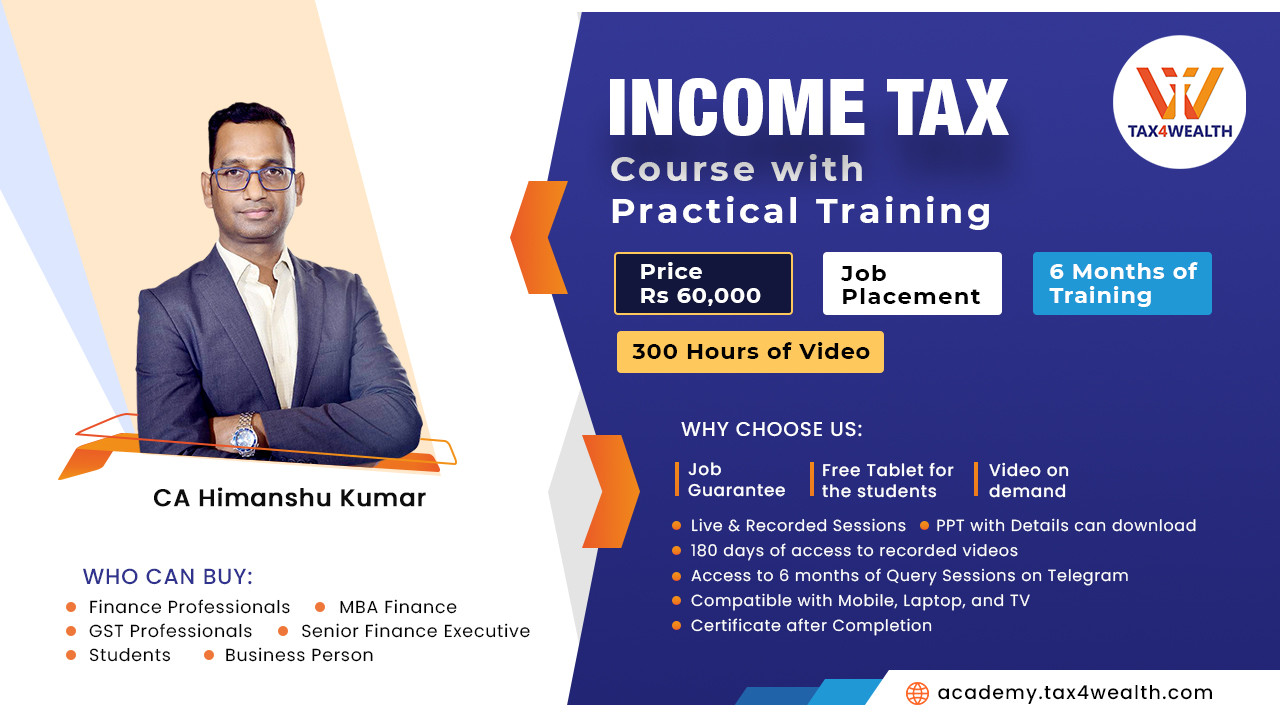

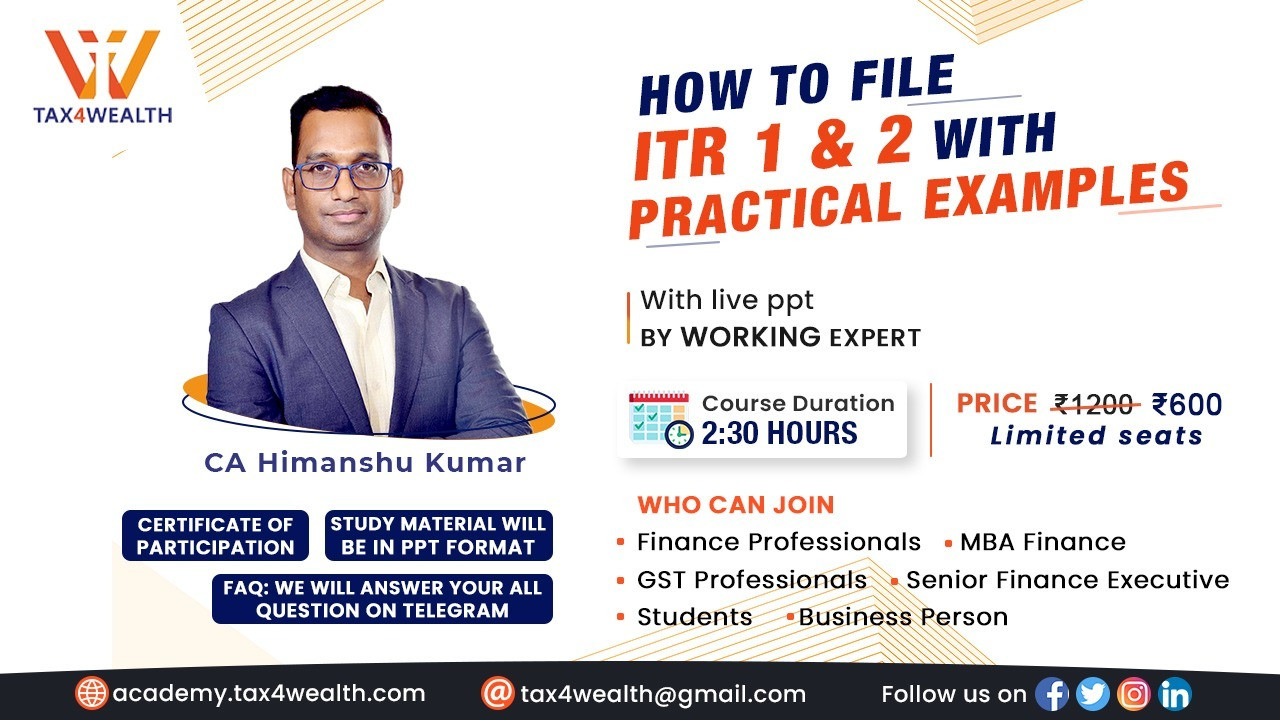

CA Himanshu

CA Praveen

Rahul

CA Himanshu

CA Himanshu

Nisha

Popular Courses.

Prakash

CA Himanshu

CA Praveen

CA Himanshu

Browse Courses By Category.

Browse Our Featured Course.

Know about Tax4wealth

Tax4wealth is an interactive platform for the video-based information related to Income Tax and Wealth Management. We are user-based content creating company wherein we have been continuously creating contents based on user feedback related to the subject.

Our Partners

Our Team, Website, and our marketing experts are our greatest assets. We are excited to provide the opportunity to the Academicians/Instructors from around the world that can join us as partners in our organization. We are here, to enhance the knowledge and provide the tools and skills to teach our users/students/professionals by providing them online video-based information related to Income Tax and Wealth Management to grow their skills at Academy Tax4wealth with CA Experts.

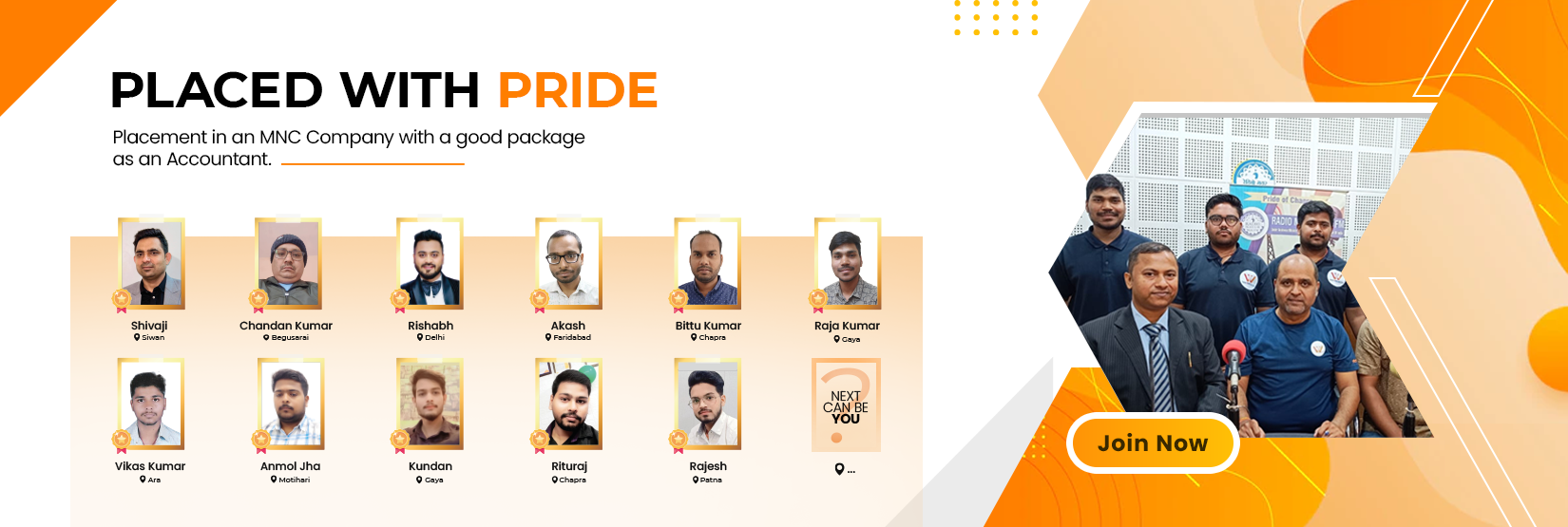

Top-Placed Students

Akash

Bittu Kumar

Chandan Kumar

Raja Kumar

Rishabh

Anmol

Vikas Kumar

Rajesh

.jpeg)

Rituraj

Hire Professionals

Our Placements Partners

Our Branches

Delhi

Under DFS Building, Annexe Building, Jeevan Vihar, Sansad Marg, New Delhi, Delhi 110001.jfif)

Patna

3rd Floor, MAX Mall, Rajapur pool Max mall, North Anandpuri, Anandpuri, Patna, Bihar 800001.jfif)

Chapra

Front of kachari Railway Station, behind Ganga Singh college, Chapra.jfif)

Gaya

AP Colony, Raj Kala bhawan 1st floor, near gaya college more, Gaya, 823001.jfif)

Muzaffarpur

In front of grand mall, kidzee campus.jfif)

Biharsharif

Sanskar Tower, A to Z chemistry, near kumar cinema, pool per, biharsharif, 803118.jfif)

Gopalganj

Pratishtha computer academy, dighwa dubuali.jfif)

Begusarai

Behind GD College, Near commerce Gyan 2nd floor, pipra, ward no 23, begusarai, 851101Get In Touch

Useful Links

Need some help?

We take our mission of increasing global access to quality education seriously.

Connect with us on Tax4Wealth

Get in touch